2026 State of the

Cloud enters the value era:

Table of contents

The fifteenth annual Flexera 2026 State of the Cloud Report sheds light on the cloud computing trends, the pressures facing IT professionals and the strategic initiatives they’re utilizing to remain competitive in today’s dynamic and evolving landscape.

This year’s report shows cloud has entered a new phase—one where value, governance and conquering complexity define success. Generative AI (GenAI) is accelerating, and hybrid cloud remains the dominant architecture. Centralization is gaining momentum as cloud centers of excellence (CCOEs) and FinOps teams expand their reach, and managed service providers (MSPs) are evolving to meet new demands. These trends underscore a clear message: Success in the cloud isn’t just about technology—it’s about aligning stakeholders to drive business value.

Report highlights

Here’s a sample of key findings from this year’s report based on a survey of 753 cloud decision-makers and users from around the world.

What are your top metrics for assessing progress against cloud goals?

N=753

Source: Flexera 2026 State of the Cloud Report ![]()

![]()

Organizations are moving beyond cost-cutting. Value delivered to business units rose 12 percentage points year over year, while cost efficiency/savings—though still in the top spot—dropped by 6 points, signaling a pivot toward prioritizing business outcomes over savings.

Use of generative Al (GenAl) public cloud services

2026: N=692, 2025: N=628; 2024: N=753

Source: Flexera 2026 State of the Cloud Report ![]()

![]()

GenAI has gone mainstream. All respondents indicate they’re using it in some capacity, and nearly half are using it extensively.

Organizations embrace hybrid cloud

N=753

Source: Flexera 2026 State of the Cloud Report ![]()

![]()

Hybrid cloud continues to lead, with 73% of organizations operating hybrid estates. Multi-cloud adoption is also rising, potentially driven by mergers or siloed applications rather than deliberate strategy.

What’s your estimated wasted cloud spend on laaS and PaaS?

N=753

Source: Flexera 2026 State of the Cloud Report ![]()

![]()

After five years of decline, wasted cloud spend increased slightly to 29%, reflecting growing cost complexity from AI and new IaaS and PaaS services.

Key findings

Cloud enters the value era

Organizations are moving beyond the early FinOps focus on costcutting. This year’s data shows a clear pivot toward measuring business value instead of just savings. Metrics like value delivered to business units jumped 12 percentage points, while cost efficiency and cost avoidance declined. This shift signals growing maturity: FinOps is evolving into a role that helps articulate the business value of technology. More teams are adopting unit economics to understand cost per service and align spending with outcomes, with nearly half (49%) using this approach, compared to only 40% last year. The message is clear: Cloud success is no longer about trimming budgets—it’s about proving ROI and enabling innovation.

AI adoption accelerates—and oversight rises

GenAI has become pervasive. In terms of public cloud services used by all organizations, GenAI has jumped 8 percentage points to the third-place spot (58%), and nearly half say they use it extensively. Large enterprises are investing heavily in governance, with 85% reporting a dedicated team or senior leader responsible for AI oversight. Organizations recognize that AI brings not only opportunity but also complexity and risk. Governance frameworks, cost visibility and automated controls are becoming essential as AI workloads expand.

IT complexity grows

Hybrid cloud remains the dominant architecture, with 73% of organizations operating hybrid estates—a 3-percentage-point increase year over year. Multi-cloud adoption also continues to inch upward, increasing by 2 percentage points from last year. Complexity is compounded by simultaneous migration and repatriation, SaaS proliferation and the rapid adoption of AI.

Cost challenges persist

Estimated wasted cloud spend ticked up to 29%, reversing a five-year downward trend. Despite clear savings, fewer than half of organizations are utilizing any one commitment discount per cloud provider. These patterns underscore the persistent challenge of managing costs in an environment where innovation and flexibility often outweigh predictability and control.

Centralization and governance gain momentum

Organizations are formalizing cloud oversight to tame complexity and align strategy. Adoption of CCOEs rose to 71%, and FinOps team prevalence climbed to 63%. Governance responsibilities are expanding beyond cloud teams to include business units and software asset management (SAM) teams, reflecting a more holistic approach to managing cloud usage and costs. This centralization trend is especially strong among enterprises, which have more resources to dedicate staff to governance and cost optimization. SMBs are catching up, but many still rely on DevOps teams for cost control. The rise of centralized governance signals that organizations see cloud as a strategic asset requiring disciplined oversight.

MSPs evolve to meet new demands

Managed service providers (MSPs) and systems integration partners remain critical for managing complexity—but with the rise of AI, their service catalog is changing. Nearly half of MSPs plan to offer AI consulting and SaaS management services, while two-thirds are adopting AI for cybersecurity use cases. Enterprise use of MSPs is up 3 percentage points year over year, but at the same time, SMB reliance has declined from 48% to 39%, likely due to budget constraints. For these partners, the ability to differentiate through advanced services—such as AI strategy and SaaS optimization—will be key to growth. For customers, services partnerships remain valuable for specialized expertise, but governance and cost accountability increasingly sit with internal teams.

Methodology

The Flexera 2026 State of the Cloud survey tapped 753 technical professionals and executive leaders worldwide in the winter of 2025. The network includes professionals across industries and context areas.

Flexera sources participants from an independent panel that’s rigorously maintained and is comprised of vetted respondents with detailed profiles. All numbers and percentages are rounded to the nearest whole number.

Reuse

We encourage the reuse of data, charts and text published in this report under the terms of this Creative Commons Attribution 4.0 International License. You’re free to share and make commercial use of this work as long as you provide attribution to the Flexera 2026 State of the Cloud Report as stipulated in the terms of the license.

SMBs

Businesses with fewer than 1,000 employees

Enterprises

Organizations with more than 1,000 employees

Large enterprises

Organizations with more than 10,000 employees

Organizations

embrace hybrid

cloud

73% of all organizations embrace hybrid cloud

The majority of organizations now use a hybrid cloud model, a figure that has increased by 3 percentage points compared to last year. Multi-cloud adoption has also risen by 2 percentage points year over year; however, just 14% of organizations surveyed operate exclusively in a multi-cloud environment without a private cloud. A 3-percentage-point growth in hybrid cloud adoption may indicate organizations are becoming more adept at monitoring and managing cloud costs.

Hybrid cloud is predominant across organizations of all sizes. Among those with up to 5,000 employees, 69% have a hybrid cloud model, while the rate increases to 78% in organizations with more than 5,000 employees. This pattern closely mirrors monthly cloud spending patterns: 68% of organizations spending up to $500,000 per month utilize hybrid cloud, compared to 79% of those with monthly spending above $500,000.

In enterprises, this hybrid situation perhaps arises from mergers or acquisitions. For example, one company might rely on Amazon Web Services (AWS) for its infrastructure, but after acquiring another business or codebase using Google Cloud Platform (GCP), they become a mixed environment. Similarly, existing private cloud setups can be combined with public cloud infrastructure when a new product is acquired.

Conversely, some organizations intentionally adopt hybrid or multi-cloud strategies to optimize workload placement. Ultimately, however, many organizations end up with complex cloud environments by happenstance rather than by design.

Interestingly, the types of multi-cloud architectures being used have changed very little. Applications isolated in distinct environments remain the leading cause for multi-cloud setups, while strategic workload placement and workload bursting are still the least common motivations.

Organizations embrace hybrid cloud

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 1) ![]()

![]()

Hybrid cloud strategies by company size

5,000 or less employees: N=386; 5,001+ employees: N=367

Source: Flexera 2026 State of the Cloud Report (Figure 2) ![]()

![]()

Hybrid cloud strategies by monthly spend

Up to $500K per month: N=358; More than $500K per month: N=374

Source: Flexera 2026 State of the Cloud Report (Figure 3) ![]()

![]()

What types of multi-cloud architectures does your company use?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 4) ![]()

![]()

Public cloud

adoption continues

to accelerate

Sixteen percent of survey respondents are spending between $200,001 and $500,000 per month on public cloud services. This remains unchanged from last year; it still stands as the most common spending range. Meanwhile, spending in the lowest three tiers has collectively fallen by 4%, while the top three tiers have seen a combined increase of 3%, indicating a shift toward higher overall cloud expenditures. The upward trend in cloud spending continues as more workloads are migrated to, or born in, the cloud.

Public cloud spending is also closely linked to company size. Sixty-nine percent of SMBs spend less than $50,000 per month on public cloud, while 76% of large enterprises spend more than $5 million each month. Most enterprises (73%) fall into the $200,001 to $500,000 monthly spending bracket. Although there are exceptions, the general trend is clear: The larger the organization, the greater its cloud spending.

76% of large enterprises spend more than $5 million on the cloud each month

Current monthly public cloud spend for all organizations

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 5) ![]()

![]()

Current monthly public cloud spend by organization size

Large enterprise: N=236; Enterprise: N=384; SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 6) ![]()

![]()

Most organizations spend between $200,001 and $500,000 per month on SaaS

Current monthly SaaS spend for all organizations

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 7) ![]()

![]()

Annual spending on SaaS mirrors trends in public cloud spending. The largest group of respondents (18%) report monthly expenditures between $200,001 and $500,000, making it the most common spending tier. In contrast, last year’s highest concentration was in the $50,001-$100,000 per month category. Spending in the three lowest tiers has dropped by a combined 7%, while spending in the top five tiers has climbed by 9% overall—demonstrating significant growth in SaaS investments.

Industry analysts support these findings: Gartner reported nearly 12% growth in SaaS spending for 2025 and forecasts an additional 15% increase in 2026.

Current monthly SaaS spend by organization size

Large enterprise: N=236; Enterprise: N=384; SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 8) ![]()

![]()

A closer look at company size shows that most SMBs (73%) spend less than $50,000 per month on SaaS. Meanwhile, 72% of enterprises fall into the $200,001 to $500,000 monthly spending bracket, and a substantial 84% of large enterprises spend more than $5 million each month. In general, just as we saw with cloud spend, SaaS spending increases with company size.

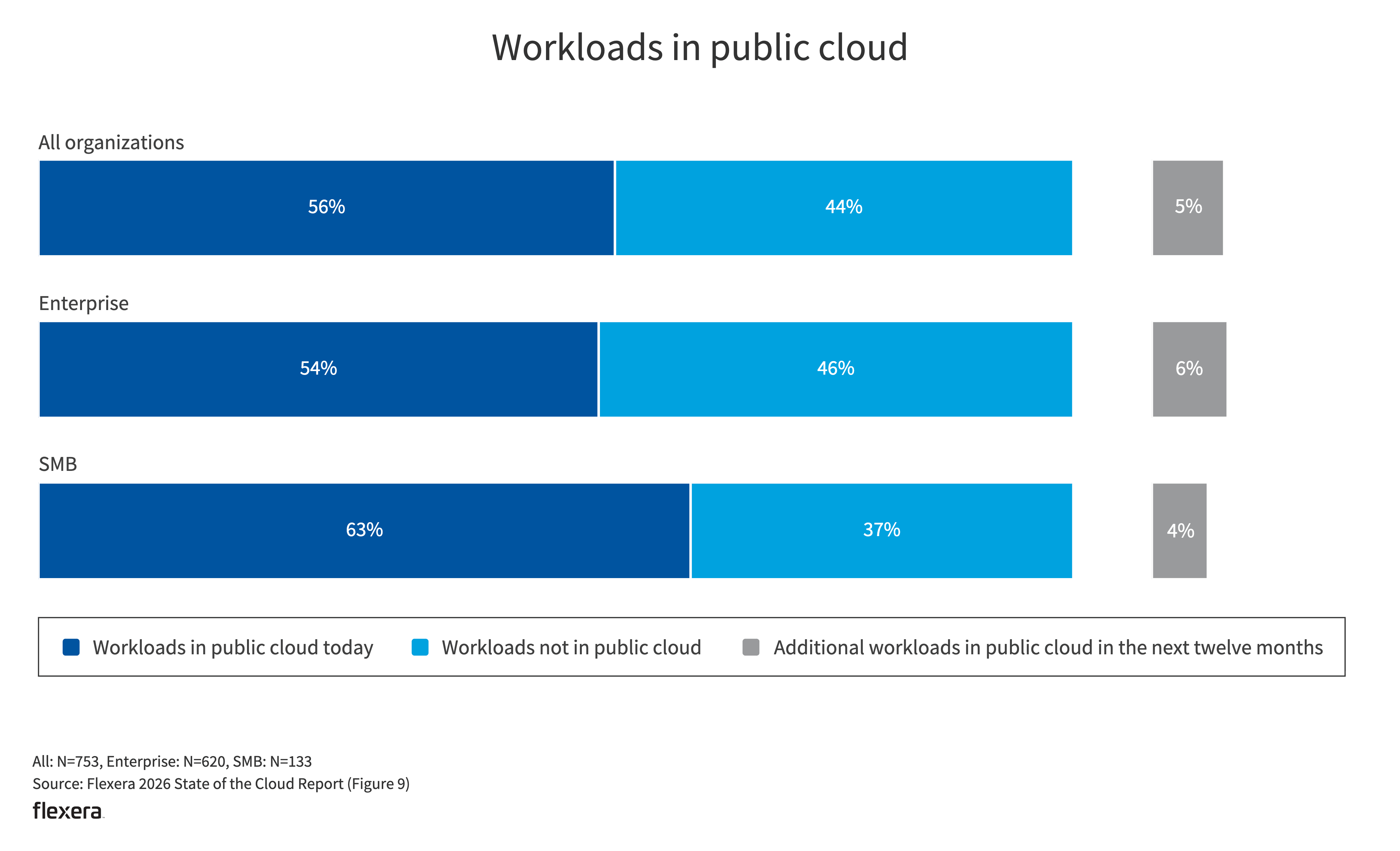

This year, the number of workloads running in the public cloud has continued to rise. Last year, SMBs anticipated a 13% increase in cloud workloads, but the actual growth jumped by 8 percentage points—still a notable gain. Enterprises saw their cloud workloads grow from 52% to 54%, while SMBs experienced a substantial jump from 55% to 63% year over year. This upward trend highlights that organizations are increasingly moving more of their operations to the public cloud.

There was little movement year over year regarding data in public cloud. The majority of SMBs (61%) and enterprises (51% ) currently have data in public cloud.

63% of SMBs have workloads in public cloud, an 8-percentage-point increase year over year

Workloads in public cloud

All: N=753, Enterprise: N=620, SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 9) ![]()

![]()

Data in public cloud

All: N=753, Enterprise: N=620, SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 10) ![]()

![]()

What percentage of cloud-based workloads have you repatriated?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 11) ![]()

![]()

What percentage of cloud-based data have you repatriated?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 12) ![]()

![]()

The percentage of cloud-based workloads and cloud-based data that organizations have repatriated each increased by 2 percentage points year over year, which may indicate that organizations are trying to leverage their hybrid cloud environment by placing workloads where it makes the most sense to run them.

What’s your approach for migrating data to public cloud/SaaS?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 13) ![]()

![]()

Organizations are increasingly confident about migrating sensitive data to the cloud/SaaS providers. While most nonsensitive data has already moved to the cloud, a growing portion of sensitive data is now also stored in the cloud or with SaaS providers—a trend that has steadily risen over the past four years.

Organizations are considering costs upfront, rather than focusing on cost optimization after migration

Understanding application dependencies and assessing technical feasibility are the top two migration challenges for all respondents, regardless of organizational size. Interestingly for all respondents, the challenge of optimizing costs after migration has fallen from third to fifth place (39%), now ranking behind assessing on-premises vs. cloud costs (43%) and selecting the best instance (40%). This indicates that more organizations are adopting a “shift left” approach with FinOps—considering costs earlier during the architectural planning phase, before cloud application deployment.

Perhaps they recognize that the traditional “lift and shift” method may not be the most cost-effective. As a result, they’re investing more effort upfront by analyzing costs, and choosing the best instances has become a bigger challenge than focusing on cost optimization after migration.

What challenges do you face in migrating workloads to public cloud?

All: N=753, Enterprise: N=620, SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 14) ![]()

![]()

Delivering

business value

grows in

importance

The leading cloud initiatives for organizations remain consistent over time. The majority of respondents (68%) rank optimizing cloud costs at the top of their priority list, though this number is down 4 percentage points year over year, followed by migrating more workloads to the cloud at 49% and better financial reporting at 42%.

However, the primary metrics used to measure progress against cloud objectives have shifted. There has been a 12-percentage-point rise in the value delivered by business units (now at 64%), a 3-percentage-point increase in competitive advantage, and a 2-percentage-point uptick in the speed of innovation. On the other hand, cost avoidance saw a slight decrease, and cost efficiency/savings dropped by 6 percentage points.

These shifts highlight FinOps growing maturity. The FinOps Foundation’s State of FinOps 2026 Report notes “FinOps is no longer just explaining past spend.” Jay Litkey, SVP Cloud & FinOps, Flexera, says that FinOps “has expanded from cloud financial management into a broader discipline focused on technology value across AI, SaaS, licensing and the data center,” reflected by the shift to metrics that prioritize value over cost reduction.

Another notable year-over-year change was in geographic reach, which climbed from 29% to 40%. Increasing geographic reach enables organizations to place data closer to users, reducing latency, and enables them to replicate it in distant locations, enhancing disaster recovery and lowering risk. It also allows for selection of data centers with high-speed networks, skilled personnel and reliable power and water, all of which contribute to better performance. Additionally, organizations can ensure compliance with regulations like the General Data Protection Regulation (GDPR). Monitoring this key metric helps guarantee that mission-critical workloads remain fast, available and protected against loss.

Modern organizations depend on technology to function, making infrastructure availability and speed critical for success. One of the most significant advantages of public cloud over private solutions or traditional data centers is the increased diversity and flexibility in data storage and replication locations. This breadth of choice empowers teams to place data where it delivers the greatest advantage, strengthening resilience and reducing latency to enable rapid scaling as business demands evolve.

64% of organizations rely on the value delivered to business units to measure progress against cloud objectives

Top cloud initiatives for all organizations

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 15) ![]()

![]()

What are your top metrics for assessing progress against cloud goals?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 16) ![]()

![]()

Organizations are

taking a centralized

approach to the cloud

Overall, a greater number of organizations now have a CCOE compared to last year, with adoption rising from 69% to 71%. Notably, SMBs saw a 6-point increase, indicating they too recognize the value of centralizing cloud strategy and are allocating staff specifically for this purpose.

Enterprises continue to be much more likely than SMBs to have a CCOE, with 76% of enterprises compared to just 49% of SMBs taking that route. While SMBs often rely on their DevOps teams for cost optimization, enterprises typically have dedicated cost management teams. That’s not surprising, since enterprises generally have more resources to hire for these roles and larger teams of developers and engineers to manage. A centralized team can create strategy and policies that keep numerous, decentralized teams aligned with corporate goals.

There was also a 4-point increase in organizations with a FinOps team focused on advising, managing and executing cloud cost optimization strategies, with numbers rising from 51% in 2024, to 59% in 2025 and reaching 63% this year. This trend reflects the growing maturity of organizations as they progress in their cloud cost management journey.

71% of all organizations have a CCOE or similar, and 63% rely on a FinOps team

Does your company have a central cloud team or CCOE to govern cloud use and set policies?

All: N=753, Enterprise: N=620, SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 17) ![]()

![]()

Does your company have a FinOps team to advise on, manage or execute cloud cost optimization strategies?

All: N=753, Enterprise: N=620, SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 18) ![]()

![]()

SAM teams are taking on a bigger role in cloud responsibilities

This year, there has been a noticeable shift in which teams govern the usage and cost of IaaS/PaaS. The majority (56%) still report that their CCOE or cloud team is responsible for these duties. However, FinOps teams saw an increase in responsibility, rising from 38% last year to 45% this year. Business units’ involvement also grew, moving from 20% to 25%, while the participation of SAM teams expanded significantly from 6% to 15% year over year.

Last year, SAM teams played less of a role in cloud cost management, with their participation remaining in the single digits. This year, however, their involvement reached double digits across the board as they took on greater responsibility for overseeing software usage in the cloud. This change underscores the growing role of SAM teams in cloud optimization efforts.

Who in your organization has primary responsibility for cloud cost management?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 19) ![]()

![]()

Utilization of MSPs for managing public cloud

All: N=753, Enterprise: N=620, SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 20) ![]()

![]()

Last year, just 6% of SMBs said they planned to reduce their use of MSPs. However, the actual figure this year was higher, with 9% of SMBs decreasing MSP usage. This notable decline—greater than anticipated—suggests the decrease wasn’t entirely strategic. It’s possible that SMBs either lacked the budget for MSP services or felt confident relying on their internal teams instead.

While some SMBs are reducing their reliance on MSPs, those continuing to work with these providers are primarily seeking essential cloud services such as security and compliance support (65%), cloud migration (64%) and FinOps (58%). Although less than half (44%) of MSPs are currently offering AI consulting, 49% of respondents say they plan to expand into AI consulting and strategy services in the future. This planned shift aligns closely with broader industry trends, as service offerings tend to evolve alongside emerging technologies and organizational needs.

Join our partner ecosystem

Get started todayWhat services are MSPs currently offering or planning to offer their customers?

N=104

Source: Flexera 2026 State of the Cloud Report (Figure 21) ![]()

![]()

Managing

cloud spend and

security remain

top challenges

It’s no surprise that cost (85%) and security (82%) continue to be the leading challenges for organizations. In fact, this marks the fourth consecutive year that cost has outranked security as the top concern, after a decade with security in the lead. Managing software licenses isn’t far behind, with 78% of all respondents ranking this in third place.

Cloud providers are continuously adding new resources and services, and cloud-based AI services are notably more expensive than traditional options. On top of that, SaaS and PaaS vendors frequently implement different pricing structures when compared to IaaS providers. These factors contribute to growing complexity, which helps explain why managing cloud spend remains a challenge—even though 63% of organizations have implemented FinOps practices.

85% of respondents say managing costs is their number one priority

Talk to an expert about optimizing your cloud costs

Top cloud challenges

All: N=753, Enterprise: N=620, SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 22) ![]()

![]()

Organizations

struggle to

control growing

cloud spend

Twenty-seven percent of respondents expect to increase their public cloud spending, while 17% reported exceeding their public cloud budgets in the past year. These trends have remained relatively stable from year to year, but as organizations adopt new resources and services, accurate forecasting remains a persistent challenge. The introduction of AI is poised to create more budget overruns.

What’s your anticipated growth on public cloud spend?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 23) ![]()

![]()

How did you perform against your public cloud budget?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 24) ![]()

![]()

What’s your estimated wasted cloud spend on laaS and PaaS?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 25) ![]()

![]()

What’s your estimated wasted public cloud software spend?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 26) ![]()

![]()

For the past five years, estimated wasted cloud spend on IaaS and PaaS has been decreasing, but this year we saw a slight uptick to 29%, and wasted cloud software spend inched up 1 percentage point, perhaps a result of the increased cost complexity brought on by AI and new PaaS/SaaS offerings. Gartner reports that SaaS spending continues to climb, yet the level of waste remains relatively constant, suggesting organizations are gaining ground on effective SaaS cost management.

With cloud spending and cost management growing more complex, provider discounts offer organizations valuable opportunities to optimize budgets and reduce overall expenses. This year, there has been a modest uptick in the adoption of commitment-based discounts—such as reserved instances (RIs) and savings plans (SPs)—across the major cloud providers: AWS, Microsoft Azure and GCP. Notably, 48% of respondents now use Google Committed Use Discounts (CUDs)—up 4 percentage points from last year—and 45% take advantage of AWS RIs, which increased by 3 percentage points. Azure RIs and SPs have also increased by 4 percentage points year over year. These programs deliver tangible savings, so the rise in their use is a positive trend. This may signal that customers are cautious about long-term commitments on these cloud platforms and are prioritizing greater flexibility.

Adoption of commitment discounts remains fragmented

Still, fewer than half of organizations are utilizing any one commitment discount per cloud provider. This may be due to the complexity and time required to manage commitment-based savings, or it could reflect a deliberate choice to maintain speed and flexibility. Many organizations prioritize innovation in the cloud, and some are reluctant to restrict engineers to specific resources, fearing it could hinder progress and innovation. The combination of commitment-discount complexity and the desire for maximum flexibility results in more than half of respondents using on-demand pricing.

Interestingly, the steepest declines in discount usage are seen with IBM and Oracle. IBM cloud subscriptions dropped by 10 percentage points to 29%, and IBM RIs saw a 12-point decrease to 26%. Oracle experienced the largest dip, with usage of universal credits falling from 39% to just 25% year over year. This could be due to the sample size combined with the smaller customer base of both clouds. As organizations progress in their FinOps maturity, we expect to see increased usage of RIs and SPs.

The use of Azure Enterprise Agreement has fallen to 43% as Microsoft phases out this program, perhaps prompting customers to transition toward the Microsoft Customer Agreement for Enterprise (MCA-E).

Which provider discounts do you use?

N=737

Source: Flexera 2026 State of the Cloud Report (Figure 27) ![]()

![]()

Usage of cloud provider discounts across all organizations

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 28) ![]()

![]()

Does your organization track SaaS costs as part of laaS/PaaS costs?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 29) ![]()

![]()

More organizations are moving toward tracking their SaaS costs as part of their IaaS/PaaS costs and moving away from tracking SaaS costs separately.

Notably, 8% of respondents said they aren’t tracking SaaS costs, an increase from last year’s 5%. Those who don’t track their SaaS costs no doubt have shadow IT—and a visibility problem. This underscores growing complexity; SaaS is proliferating, but a growing number of organizations aren’t tracking the cost.

8% of respondents aren’t tracking SaaS costs—opening the door to shadow IT

Discover how to take control and eliminate shadow IT with Flexera One

Organizations tracking a unit metric increased 9 percentage points year over year

Does your organization track a unit metric to improve unit economics?

All: N=753, Enterprise: N=620, SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 30) ![]()

![]()

Organizations seek to gain more granular visibility into their cloud expenditures so they can better understand the value these investments deliver. By analyzing unit costs, companies can make more informed decisions about cloud and SaaS spending returns. Enterprises (53%) are much more likely than SMBs (32%) to measure unit economics; they likely have more dedicated resources to establish the data pipeline and track a unit metric.

Usage of

top public cloud

providers remains

consistent

What’s your usage of the following public cloud providers?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 31) ![]()

![]()

The neck-and-neck battle for dominance between AWS and Azure continues. Both organizations are being used in some capacity by 88% of respondents. AWS (83%) pulls slightly ahead of Azure (79%) if considering those who are currently running some or significant workloads in the cloud.

83% of respondents are running significant or some workloads in AWS, compared to 79% using Azure

YoY public cloud provider usage by all organizations

2026: N=753, 2025: N=759

Source: Flexera 2026 State of the Cloud Report (Figure 32) ![]()

![]()

77% of SMBs currently run some or significant workloads with AWS, their preferred cloud provider

Currently, AWS holds a slight edge for active enterprise workloads, with 84% compared to Azure’s 82%. However, when factoring in organizations that are experimenting or have future plans, Azure moves ahead with 94%, while AWS trails at 92%.

For SMBs, AWS continues to be the preferred choice: 77% are currently running some or significant workloads with AWS compared to 63% using Azure. For all organizations GCP remains firmly in third place but lags significantly behind the two frontrunners.

Enterprise use of public cloud providers

N=620

Source: Flexera 2026 State of the Cloud Report (Figure 33) ![]()

![]()

YoY enterprise use of public cloud providers

2026: N=620, 2025: N=622

Source: Flexera 2026 State of the Cloud Report (Figure 34) ![]()

![]()

SMB use of public cloud providers

N=133

Source: Flexera 2026 State of the Cloud Report (Figure 35) ![]()

![]()

YOY SMB use of public cloud providers

2026: N=133, 2025: N=137

Source: Flexera 2026 State of the Cloud Report (Figure 36) ![]()

![]()

Cloud spending mirrors usage, so it, too, has remained largely unchanged year over year, with AWS and Azure continuing their close competition for the top spot. There’s no clear trend indicating that either provider will become the dominant choice in the near future.

Use of Azure showed the most year-over-year change in the $500,001 to $1 million per month tier (7% in 2025 to 11% in 2026), and use of AWS showed the most change in the $200,001 to $500,000 per month bracket (10% in 2025 to 14% in 2026).

How much do you spend on each cloud provider?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 37) ![]()

![]()

Enterprise public cloud spend

N=620

Source: Flexera 2026 State of the Cloud Report (Figure 38) ![]()

![]()

SMB public cloud spend

N=133

Source: Flexera 2026 State of the Cloud Report (Figure 39) ![]()

![]()

How many VMs do you have in each cloud provider?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 40) ![]()

![]()

AWS, Azure, GCP and Oracle are closely matched when looking at small deployments of virtual machines: roughly a quarter of respondents have 1-50 instances with each provider, and 17% of respondents have a small (1-50 instance) deployment at IBM.

Azure (22%) has the lead for 51-100 instance deployments, followed by AWS at 18% and GCP at 16%.

For larger deployments of 101–1,000 instances, AWS and Azure are close (14% and 13% respectively), while GCP dips in this category to 7%.

When looking at the largest VM deployments (over 1,000 instances), AWS has the lead. Eleven percent of respondents indicated that they have more than 1,000 VMs with AWS. Eight percent have a deployment this size with Azure. Only 5% have a 1,000+ instance deployment with GCP.

GenAI has the

largest increase

in usage across

public cloud

services

Public cloud data warehouse usage dipped slightly to 71% after peaking at 74% last year. This decline may be due to prominent third-party vendors like Snowflake and Databricks capturing substantial market share from the major public cloud vendors.

Today, nearly every organization is leveraging some form of AI or machine learning (ML). Among public cloud services, current usage of GenAI saw a notable jump, rising from 50% to 58%. Non-GenAI/ML usage also grew, increasing from 49% to 52%. Meanwhile, current use of search services dropped from 55% to 49%.

Public cloud services used by all organizations

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 41) ![]()

![]()

Use of generative Al (GenAl) public cloud services

2026: N=692, 2025: N=628; 2024: N=753

Source: Flexera 2026 State of the Cloud Report (Figure 42) ![]()

![]()

As GenAI becomes integrated into daily workflows, its applications are taking shape—from helping engineers write code and assisting operations teams with management tasks, to answering consumer questions. Whether application developers or business leaders, all respondents report that they now utilize some form of GenAI service offered by public cloud providers. Forty-five percent of respondents say they’re using GenAI extensively, up from 36% last year. Thirty-six percent say they use it sparingly, and 18% indicate they’re experimenting.

All survey respondents indicate they’re using GenAI in some capacity; 81% are using it extensively or sparingly

47% of large enterprises have a dedicated AI governance team or leader

While AI initiatives are most often overseen by an IT leader or head of cloud strategy, large enterprises—those with more than 10,000 employees—are much more likely to establish a dedicated AI governance team. This makes sense: Larger enterprises have the resources to allocate specialized staff, and with greater investments in AI, robust oversight becomes increasingly important.

Managing AI workloads isn’t without its challenges, however. In fact, it’s reminiscent of the top challenges organizations faced in the early days of cloud: Dynamic usage makes it hard to forecast costs. Rightsizing resources for both cost and performance remains a delicate balance, and new pricing metrics make cost visibility and optimization a challenge all over again.

One key difference now is that organizations feel they have the FinOps knowledge and frameworks they need to tackle these costs—only 12% of respondents said that lack of AI-specific FinOps skills and frameworks were a challenge. FinOps has had some time to take hold in organizations, so they’re prepared to manage dynamic workloads with usage-based pricing.

Who oversees your Al cloud initiatives?

Large enterprise: N=236; Enterprise: N=384; SMB: N=133

Source: Flexera 2026 State of the Cloud Report (Figure 43) ![]()

![]()

Top challenges managing Al workload costs

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 44) ![]()

![]()

Scaling AI workloads in the cloud isn’t just about technology—it’s about trust, talent and clarity. Security and compliance risks lead the list, with 53% of respondents ranking it as their number one challenge, underscoring the importance of governance and risk management. Forty percent of respondents say data quality for AI model training is their top challenge, indicating organizations struggle to ensure reliable, high-quality data pipelines for AI workloads.

Skills gaps and cost unpredictability are equally cited as the top challenge by 30% of respondents. This underscores the dual hurdles organizations face: both a shortage of talent and the complexities of managing unpredictable costs.

Integration and identifying high-value use cases also become critical as organizations move beyond experimentation. These findings reinforce the need for strong governance frameworks, robust data strategies and mature FinOps practices to manage complexity and risk.

Interestingly, 50% of respondents chose “other” for their top challenge. “Other” could include multiple obstacles, including challenges in implementing AI/ML observability and model performance at scale, multi-region or multi-cloud complexity, data transfer bottlenecks and egress costs, complexities with workload scheduling or even workflow orchestration challenges. This is something we intend to investigate further in future reports.

53% of respondents say security and compliance risks associated with cloud-based AI are their top challenge

Top three challenges facing organizations when scaling Al workloads in the cloud

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 45) ![]()

![]()

The evolving role

of sustainability

in cloud strategies

59% of organizations either have or plan to have a defined sustainability initiative within the next year

European requirements for corporate carbon reporting—the Corporate Sustainability Reporting Directive (CSRD)—have relaxed over the last few years. Deadlines have been pushed out, which means tracking carbon emissions has taken a bit of a back seat, which could explain some of the decline in sustainability initiatives. In 2024, 48% of respondents said they have a defined sustainability initiative that includes carbon footprint tracking; last year this number dropped to 36% and this year it increased slightly to 38%.

Not much has changed year over year when it comes to cloud cost optimization and sustainability prioritization. Cost optimization continues to take priority over reducing carbon emissions, though for nearly a third (30%) of respondents, the two are equal priorities.

Does your organization have a defined sustainability initiative that includes carbon footprint tracking of cloud use?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 46) ![]()

![]()

Cloud cost optimization and sustainability prioritization

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 47) ![]()

![]()

56% prioritize cost optimization over sustainability, but 30% prioritize the two equally

Get auditable visibility at the intersection of multi-cloud usage, cost and carbon emissions with Flexera One Sustainability

European

Spotlight

The majority (22%) of European respondents are from large enterprises with more than 10,000 employees. Most European respondents are in the financial services industry (30%) and 22% are in a tech-related industry. Thirty-seven percent are IT/Cloud architects, and 47% work in a CCOE or similar. Nearly half (46%) are from the UK, followed by Germany (19%).

European respondents by organization size

N=178

Source: Flexera 2026 State of the Cloud Report (Figure 48) ![]()

![]()

European respondents by industry

N=178

Source: Flexera 2026 State of the Cloud Report (Figure 49) ![]()

![]()

European respondents by role

N=178

Source: Flexera 2026 State of the Cloud Report (Figure 50) ![]()

![]()

European respondents by where in the organization they work

N=178

Source: Flexera 2026 State of the Cloud Report (Figure 51) ![]()

![]()

European respondents by country

N=178

Source: Flexera 2026 State of the Cloud Report (Figure 52) ![]()

![]()

European vs. North American use of CCOE teams

Europe: N=178; North America: N=472

Source: Flexera 2026 State of the Cloud Report (Figure 53) ![]()

![]()

Europe and North America look quite similar when asking about their usage of a CCOE team. The majority have one, and another 13% plan to add one in the next year.

European usage of FinOps teams is up 9 percentage points year over year

European vs. North American use of FinOps teams

Europe: N=178; North America: N=472

Source: Flexera 2026 State of the Cloud Report (Figure 54) ![]()

![]()

This is the same when looking at European usage of FinOps teams: The majority have one, and 14% plan to add one in the next year. It’s notable that for last year, only 56% of European respondents reported having a FinOps team while this year, 65% have one—a 9-percentage-point increase year over year.

Similar to global results, 52% of European respondents ranked understanding application dependencies as their top cloud migration challenge, followed by assessing technical feasibility (46%) and post-migration cost optimization (43%).

Cloud migration challenges for European organizations

N=178

Source: Flexera 2026 State of the Cloud Report (Figure 55) ![]()

![]()

Cloud initiatives for European organizations

N=178

Source: Flexera 2026 State of the Cloud Report (Figure 56) ![]()

![]()

Although AWS and Azure remain fairly tied for public cloud usage rates among global respondents, over half (52%) of European respondents are running significant workloads on Azure, followed by AWS at 41%.

Public cloud provider usage for European organizations

N=178

Source: Flexera 2026 State of the Cloud Report (Figure 57) ![]()

![]()

European reporting requirements have historically been the primary force behind global sustainability initiatives, initially mandating that all organizations with data in the EU report their carbon emissions. Over the past year, however, these regulations have faced delays and revisions, and now only the largest organizations are required to report. Despite these changes, the percentage of European respondents with defined sustainability initiatives has risen from 43% last year to 47% this year.

Gain actionable insight into your multi-cloud operations, costs and environmental impact with Flexera One Sustainability

Does your organization have a defined sustainability initiative that includes carbon footprint tracking of cloud use?

Europe: N=178; North America: N=472

Source: Flexera 2026 State of the Cloud Report (Figure 58) ![]()

![]()

Utilization of MSPs for managing public cloud for European organizations

Europe: N=178; North America: N=472

Source: Flexera 2026 State of the Cloud Report (Figure 59) ![]()

![]()

Although 7% of European respondents indicated last year they plan to use an MSP, the number of respondents using one has remained relatively flat year over year. Fifty-eight percent of European respondents currently use an MSP for managing public cloud, up from only 57% last year.

Cloud success hinges

on governance, value

and AI oversight

Cloud has shifted into a new phase. Organizations are no longer satisfied with simply cutting costs. They’re measuring business outcomes, adopting unit economics and shifting FinOps practices to influence decisions before workloads ever hit the cloud. This evolution reflects the recognition that the cloud isn’t just infrastructure—it’s a strategic lever for innovation and competitive advantage.

At the same time, complexity is multiplying. Hybrid remains the dominant architecture, and multi-cloud adoption continues to rise, often unintentionally. SaaS proliferation, underused discounts and the resurgence of wasted spend underscore the challenge of managing costs in an environment where flexibility often trumps predictability. These trends make governance more critical than ever. CCOEs and FinOps teams are expanding their reach, pulling in business units and SAM teams to create a unified approach to oversight.

GenAI adds another layer of opportunity and risk. Adoption is accelerating, but so is the need for control. Large enterprises are leading the way with dedicated governance teams, while security and compliance risks top the list of challenges to scaling AI workloads. Organizations that institutionalize AI oversight now will be better positioned to harness its potential without sacrificing trust or transparency.

MSPs and systems integrators remain part of the story, but their role is shifting. As SMB reliance declines, these partners are pivoting toward advanced services like AI consulting and SaaS management. For customers, these partnerships still matter, but internal governance and cost accountability are becoming non-negotiable.

Success in 2026 and beyond will hinge on maximizing value, effective oversight and managing complexity. Organizations that approach FinOps strategically, embrace disciplined discounting and establish robust AI controls will not only keep costs in check, but they’ll also unlock the full potential of cloud to fuel growth, resilience and innovation.

Demographics for all organizations

62% of respondents are from the U.S.

Twenty-two percent of survey respondents are from large enterprises with more than 10,000 employees, while 51% represent enterprises and 17% are from SMBs. Most respondents are based in the U.S. (62%), with 23% from Europe and 13% from the Asia-Pacific region.

What size is your organization?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 60) ![]()

![]()

Where are your headquarters located?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 61) ![]()

![]()

In terms of roles, 37% work in IT or operations, while 23% are cloud architects. Almost half (49%) are part of a CCOE or a similar group. Twenty-two percent of respondents come from the financial services industry, and 32% represent technology- related industries.

What’s your company industry?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 62) ![]()

![]()

What’s your role?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 63) ![]()

![]()

49% work within a central cloud team

Where in the organization do you work?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 64) ![]()

![]()

What’s your involvement with the cloud in your organization?

N=753

Source: Flexera 2026 State of the Cloud Report (Figure 65) ![]()

![]()

A significant majority (82%) participate in decisions related to public cloud IaaS/PaaS, and nearly as many (81%) are involved in choices regarding cloud software, including SaaS, cloud marketplaces or licensing.

About Flexera

Flexera helps organizations understand and maximize the value of their technology, including the rising costs and risks introduced by AI, saving billions of dollars in wasted spend. Our Flexera One platform connects the dots between what technology you have, how it is used, what it costs, and where it creates risk, helping teams take control of the increasingly complex IT estate across cloud, SaaS and on-premises. We are leading the way to unify IT asset management, FinOps and SaaS management with high fidelity data from Technopedia, our proprietary reference library of technology asset data, and intelligent automation fueled by AI. That’s why thousands of global organizations rely on the Flexera One platform and Technopedia.

Contact Flexera

NEXT STEPS